In the ruin problem with stochastic investment, we consider the following SFPE

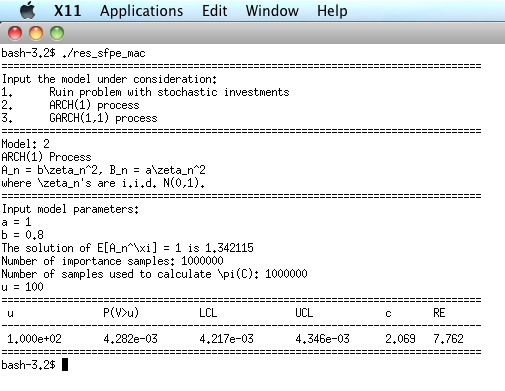

The ARCH(1) process is modeled by by the recurrence equation

The GARCH(1,1) process is modeled by by the recurrence equation

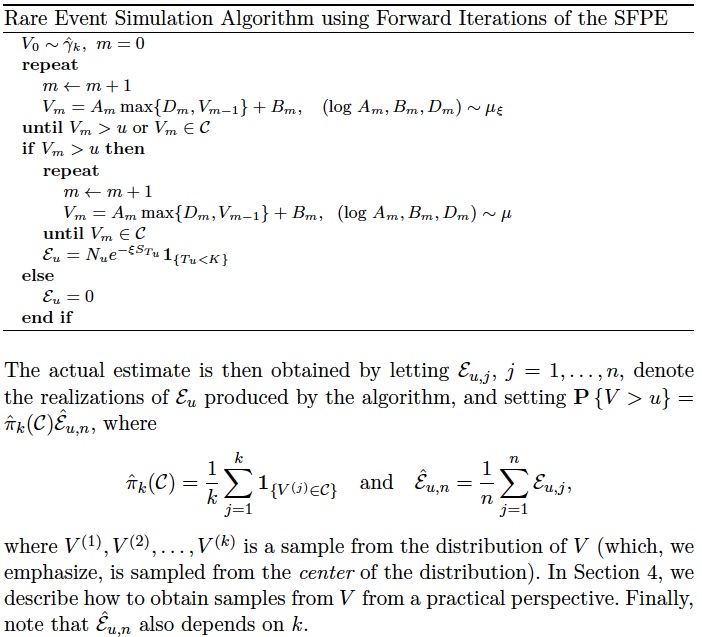

RESSFPE implements the importance sampling algorithm for estimating rare event probabilies arising from stochastic fixed point equations, as described in Collamore, Diao, and Vidyashankar ( Annals of Applied Probability, 2013).

The program is written in C language. Executable file for Linux/Mac platform is available in the download section below.

On Linux systems:

res_sfpe_linux

On Mac systems:

res_sfpe_mac

The program implements the importance sampling algorithm for estimating the tail probabilities for three types of processes: (1) ruin problem with stochastic investments; (2) ARCH(1); and (3) GARCH(1,1).

In the ruin problem with stochastic investment, we consider the following SFPE

The ARCH(1) process is modeled by by the recurrence equation

The GARCH(1,1) process is modeled by by the recurrence equation

| Model | Parameters |

|---|---|

| Ruin problem with investment | |

| ARCH(1) | |

| GARCH(1,1) | |

To estimate the tail probabily P(V>u), besides the model parameters in the above input section, one also needs to specify: (1) k; (2) n; and (3) u.

Computational results include the adjustment coefficient such that

, the tail probability

P(V>u) and its 95% confidence limits, and the relative error.